Research

The Human Value Gap in M&A

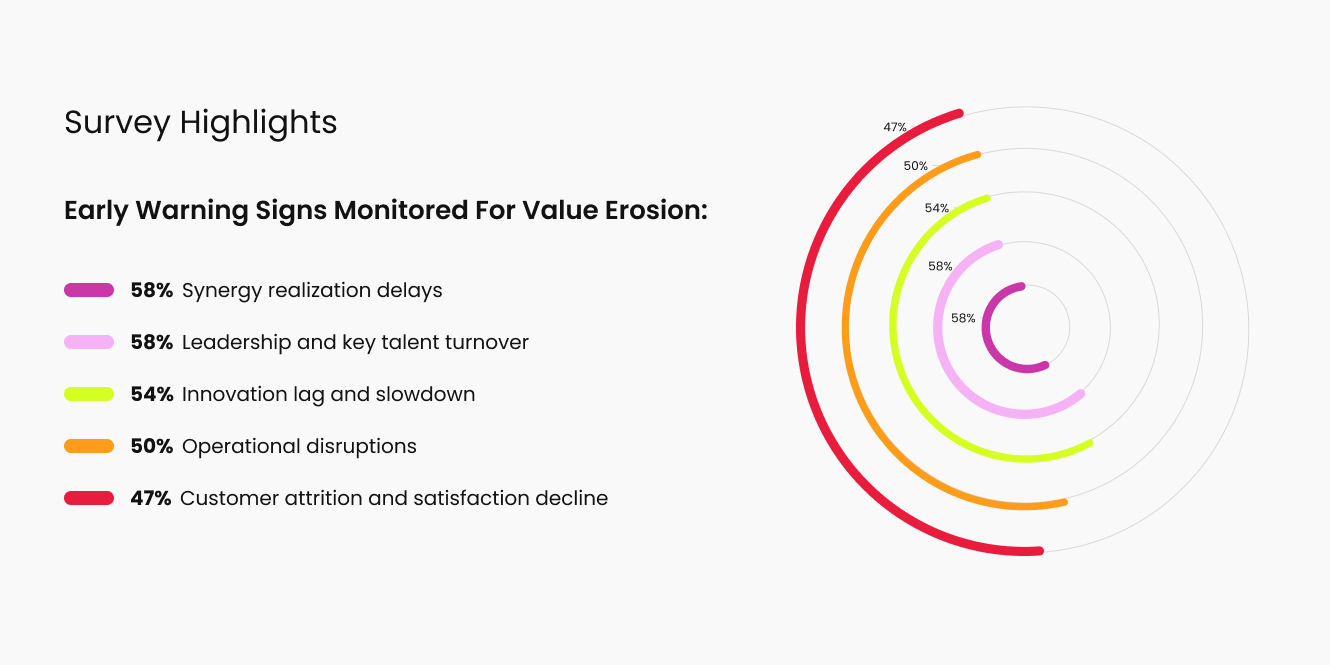

Nearly 60% of CFOs are watching for synergy delays and talent turnover after a deal closes. Our latest research reveals what those warning signs are really telling you.

Subscribe to Mindshift, RGP’s LinkedIn Newsletter

Tap into bold, visionary insights crafted for leaders like you navigating challenges and turning them into opportunities. Each issue delivers fresh ideas, real-world strategies, and expert perspectives to inspire your next move and architect a brilliant future.